From the Executive Director: Week of February 15

16 Feb 2021, by Kristin Cundiff Share :

The Senate Local Government and Taxation Committee will hear Senate Bill 1108 on Thursday at 3:00 pm MST. The IAC Legislative Committee has been reviewing the bill and will take a position tomorrow. Senate Bill 1108 is much better than Senate Bill 1021 or 1048, but there will still be a fiscal impact on local governments. Cities will likely be hit the hardest by the changes. The impact on counties will vary depending on levels of new construction. The bill proposes the following:

- All taxing districts will be allowed to increase base property tax budgets by up to 3% a year.

- Taxing districts will continue to budget new construction; however, a new formula will be used to calculate new construction.

- Rather than applying the prior year levy rate to the new construction roll, taxing districts will first compute a current year levy rate reflective of the district’s respective base budget increase.

- This new levy rate will then be applied to the new construction roll rather than using the prior year levy rate.

- A taxing district may budget up to 75% of their new construction amount. The remaining 25% will simply go to the base market value to further reduce overall levy rates.

- For new construction associated with the termination of a revenue allocation area, the district may only budget 50% of the new construction associated with the revenue allocation area. The remaining 50% will simply go to the base market value to further reduce overall levy rates.

- A taxing district can budget forgone property taxes only if its annual budget increase is less than 4%. Under this scenario, the district’s property tax budget increase would be capped at 4%.

- Property tax budget caps can be exceeded by a simple majority vote for a two-year override or by a super majority 66 ⅔ vote for a permanent override.

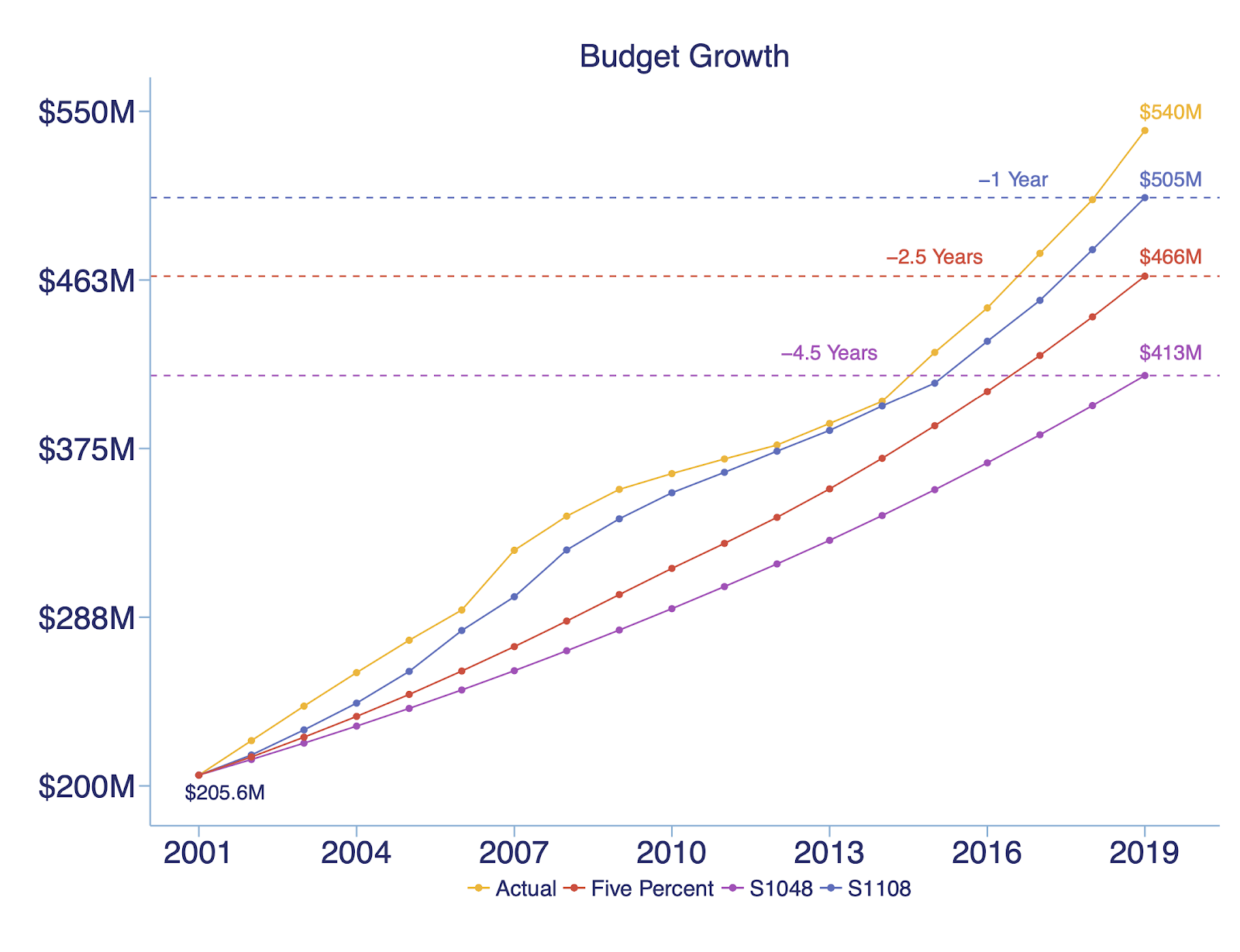

IAC has analyzed county property tax budgets back to 2001 and created a hypothetical model to establish a fiscal impact assuming Senate Bill 1108 was in place in 2001. Under our analysis, IAC found that statewide, overall county property tax budget capacity would have been reduced by a total of $34.8M or 6.54%. Essentially, had Senate Bill 1108 been in place in 2001, county property tax budgets would be set back by one fiscal year. For 13 counties, there would be no negative fiscal impact. For twelve counties, overall property tax budget capacity would have been reduced by 1% or less. Eleven counties would have seen property tax budget capacity reduced by between 1-5% while eight counties would have seen property tax budget capacity reduced by more than 5%.

IAC also analyzed a hypothetical scenario in which Senate Bill 1048 had been in place as well as a scenario in which a 5% cap was in place. Under both of these alternatives, overall county property tax budget capacity would have been greatly reduced. Under Senate Bill 1048 county property tax budget capacity would have been reduced by $127M or 30.8%. This would have set county property tax budgets back by four and a half years. Under a hypothetical 5% cap, county property tax budgets would have been reduced by $74 million or 15.9%. Under this scenario, county budgets would have been set back by two and a half years. The chart below visualized the estimated aggregate impact to counties of the three scenarios when compared to actual county property tax budgets for fiscal year 2020.

While Senate Bill 1108 is not ideal, it is the best of the alternatives currently before the legislature. Please take a look at Senate Bill 1108 and how it would impact your county budgets. Please share this information with your representative to the IAC Legislative Committee so that your voice can be heard. Also, don’t hesitate to reach out to me with any questions or comments.